Measuring the measuring stick

Humans are funny creatures. We proclaim high values and ideals, but we often lose sight of them in the daily grind of reality. Bitcoiners are no exception. In one breath we talk about how bitcoin “fixes the money” and in another, we fret over how bitcoin measured in terms of that broken money fails to meet our expectations.

Like almost every other bitcoiner I know, I find myself worrying about the fact that bitcoin is more than 50% off its latest ATH. I look at charts, read tea leaves, navel gaze, clutch my pearls, seek solace from people with more wisdom and experience than me, conduct seances to try and summon the spirit of Satoshi... all trying to figure out if bitcoin is hammering out a bottom, whether this is the final capitulation, and working on my 37th draft of bitcoin’s eulogy.

This is how I feel in every bear market but at some point (like today), I dunk my face in cold water, take a long walk, and try to reframe my thinking.

The day-to-day, week-to-week vacillations of bitcoin’s dollar price can be stressful, but mostly it’s just distracting. In short, bitcoin spent the past week doing pretty much the same thing it has done all month. It bounced around in the low sixties, tickled the upper fifties, popped to the mid-sixties on a weak U.S. jobs report, and closed the week again in the lower band of its 200-week moving average. (It’s worth remembering what happened the last time Trump got an unflattering jobs report. He humiliated and then fired the head of the BLS and called the numbers rigged.)

The weekly price oscillation can take our attention away from bigger, more interesting questions about bitcoin. I’m going to scratch at a few of them here.

Does the 200WMA matter and if so, why?

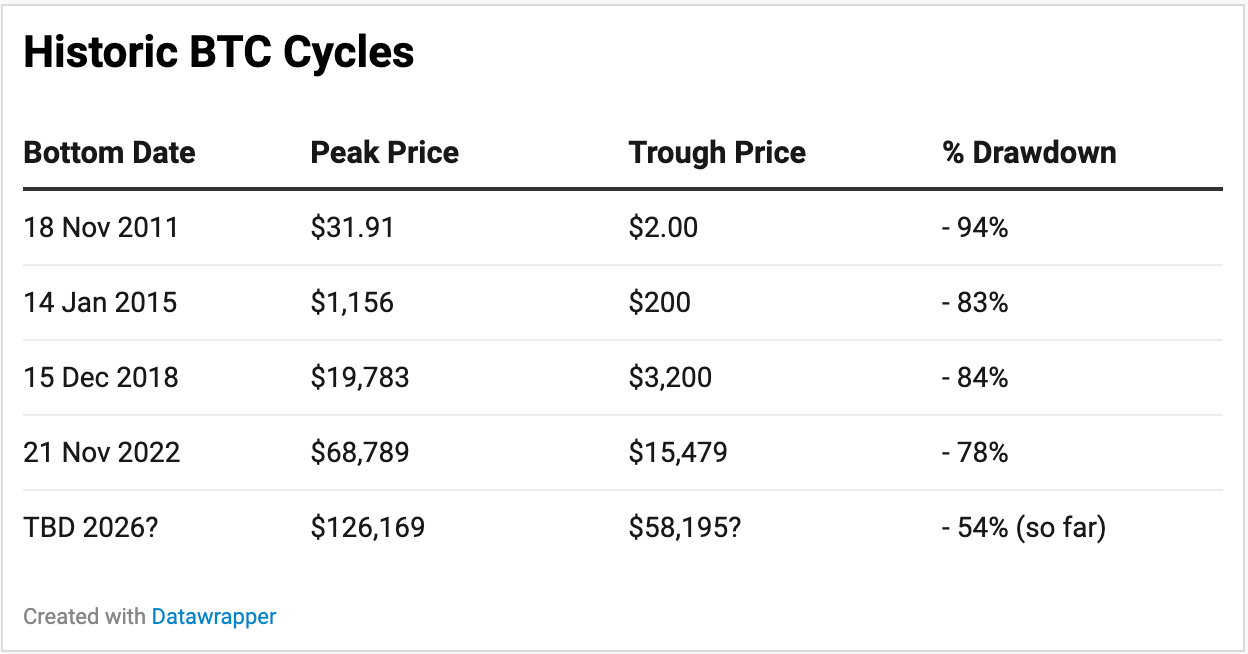

The 200-week moving average is the closest thing bitcoin has to a structural floor — it generally works out to a rolling four-year average of bitcoin’s price in USD. For as long as bitcoin has had an agreed-upon market price, the 200WMA has roughly correlated to the price zone where bear markets end and buyer accumulation begins. This week, bitcoin closed below the 200WMA for the first time this cycle. What does this suggest?

Bitcoin has only closed below the 200WMA a few times in its history. Bitcoin’s earliest crashes — in 2011 and 2015 — bitcoin either wasn’t 200 weeks old or the data was too inaccurate to provide a meaningful point of reference. But by 2015, 2018, a few days in March 2020 (COVID flash crash), and the epic, enduring trauma of the 2022 market the turning point of the crash was marked by bitcoin’s dip below the 200WMA. Each of those seasons of pain proved to be an opportunistic buying zone, not a funeral. (I burned the eulogies I wrote in 2018 and 2022.) Today we’re at about a 54% reversal.

Even as the percentage drawdowns get at least a little shallower, the economic pain in dollar terms is profoundly greater. The chart below shows the USD value of bitcoin each time Mr. Market shat the bed:

Sit with this for a moment. Unless you’re hard core anti-bitcoin (which makes me curious why you’re reading this) — and unless you’re Satoshi Nakamoto with basically free bitcoin, is there any previous market bottom you wish you missed? Yes, it hurts a lot more in dollar terms to see your $69,000 bitcoin fall to $15,000 (I was there) than it hurt to watch it go from $32 to $2. But two things stand out to me.

First — and sorry to be glib — it’s only a loss when you “recognize” it. Until you convert bitcoins to dollars, you still have the same number of bitcoins. It’s just that the external measuring stick you’re using is skewing your perspective. (See below.) If you are holding bitcoins and you need dollars, the price matters a lot. If you’re holding dollars and you’d like bitcoin, the trough should present a tempting opportunity.

Second, the current drawdown isn’t nearly as deep as in previous cycles. Yes, we’re around the 200WMA but the pullback (so far) is quite a bit shallower in percentage terms than any prior bear cycle. This might mean that we’re still a fair way from the bottom and the 200WMA is more of a coincidental correlation than a meaningful indicator. It might also mean that bitcoin is maturing as an asset class and that as time advances, we’ll see (at least nominally) lower volatility from peak to trough. (It could surely also mean any number of other things I’m not thinking about.)

The 2022 market sucked even worse than this one. Bitcoin dropped below its 200WMA in June 2022 and didn’t reclaim it until October 2023. Sixteen months of acute pain! Bitcoin was dead. TradFi was dunking on everyone in the space. The Earth crashed into the Sun and it was all over. Then came 2024. A slew of ETPs with tens of billions of dollars of retail inflows. A perceived “benevolent” administration wins election. (Don’t kid yourself.) Institutional bitcoin allocations. By 4Q2025 bitcoin ripped to its all time high over $126,000.

The point of all this is that “closing below the 200-week moving average” has historically been the sign of a bottom being hammered out. How long the bottom will last is a separate question, but I’m not yet ready to call a priest to administer bitcoin’s last rites.

Bitcoin’s presence in the market is certainly more mature than it’s ever been. Of course, this can be said of each of bitcoin’s prior cycles. New buyers enter with idiosyncratic expectations, sellers exit with theirs. As the market expands, a widening ring of allocators enter with new motives and mindsets. With large institutional allocations, bitcoin spot and futures ETPs, and the asset squarely sitting in the Overton window, perhaps we’re entering the final era of bitcoin coming of age into traditional markets.

If that’s the case, will a more mature market treat the 200WMA as a firmer floor, and resume allocation? Or will the countervailing market headwinds — war in Iran, higher interest rates, continued AI speculation — extend the pain or push it deeper?

Unfortunately, we can only wait and see.

Who’s selling

The spot bitcoin ETPs just posted the bloodiest month on record with roughly $4.5 billion of net outflows in June. The hemorrhaging continued into July even as price seemed to be recovering a little. It’s potentially an interesting data point that even as the Wall Street bitcoin products were net sellers, bitcoin’s price went up anyway.

As James Check (Checkmatey) suggests, some of the outflow is likely to manage end-of-quarter rebalancing — pension and model-based portfolios trimming positions, not necessarily a shift in investment thesis. A more interesting point of data is who isn’t selling. When you look at the capitulating coins by the seller’s tax basis, the overwhelming number of sellers are holders who bought the top of the 2025 market. Roughly 70% of realized losses come from coins bought between $70,000 and $85,000, and another 20% from above $85,000. These are most likely low-conviction buyers with weak hands, but there could certainly be some strategic sellers harvesting capital losses to offset gains elsewhere. Long-term, low-cost-basis holders have barely flinched. Coins bought below $58,000 account for less than 7% of all bitcoins changing hands in the past month.

There is no on-chain evidence indicating that long-term bitcoin holders are capitulating. By looking at aging coins on chain we can see that it’s recent buyers who have been shaken out of the market. Experienced hands are holding fast. This is a normal, healthy feature of a market bottoming process. (I strongly recommend curious readers check out the incredible work of Checkmatey, his former team at Glassnode, and other on-chain analysts in the space.)

The point I think I’ll close this section with is the advice I have given to countless others. Don’t buy bitcoin with your lunch money. Don’t buy bitcoin if you’re going to want dollars within the next four years. (And probably longer.) It is wickedly volatile and it can break your heart as quickly as it can dazzle your eyes. If you are measuring bitcoin’s success in a near-horizon dollar context, you’re more likely to be disappointed than pleased.

Strategy finds the limit of their model

For two years, Michael Saylor ran the simplest flywheel in finance: issue paper, buy more valuable assets (bitcoin), hodl, repeat. This week Strategy (MSTR) discovered that the flywheel has a limit.

As an asset, bitcoin has no margin call. Sitting in custody (self-managed or qualified), bitcoin cannot be forcibly sold. But leveraged bitcoin absolutely has a breaking point, and Strategy found it. The relevant mechanism for MSTR is its mNAV — the ratio between MSTR’s market value and the value of the bitcoin it holds. When mNAV is above 1, issuing new stock to buy more bitcoin makes shareholders richer. When it falls below 1, as it did on June 26, the flywheel grinds and starts to reverse. If mNAV is below 1, issuing new stock to buy bitcoin erodes shareholder value. Strategy was forced to do what they said they’d never do and authorized a program to sell up to ~20,000 BTC (about 2.5% of its stash) to fund its dividends and create a cash buffer.

I’m not here to dunk on Saylor and the Strategy team. The important point is NOT that they sold bitcoin when they said they’d hold it forever — chalk that up to “laser-eyed” marketing hyperbole. The important point is that they adapted to protect investors’ dividend, and the market rewarded MSTR with a healthy bounce. Even more important is that the bitcoin market was just fine as well.

But this is an example of how leverage can painfully unwind in a bear market. Title-held bitcoin can grind along indefinitely even when it hurts to watch. Leveraged bitcoin inevitably reaches its breaking point, often at the most inconvenient time. I would always prefer to be an opportunistic buyer than a forced seller. Ten times out of ten.

Crypto policy isn’t “red v. blue”

If you only focused on headlines, you’d think crypto policy in the U.S. is stuck. President Trump is holding a bill that would ban government-issued CBDCs hostage as a point of leverage to get Congress to pass a bill expanding voter ID requirements. While voter identification issues (like so many) is highly partisan and contentious, the same is not true when it comes to crypto legislation. The anti-CBDC bill passed the Senate 85–5 and the House 358–32. The CLARITY Act has also advanced with broad bipartisan support.

The gridlock in D.C. is about political dealmaking, not opposition to the policy. Despite Republican and Libertarian candidates making the rounds at Bitcoin conferences and sightings of red hat-wearing bitcoiners and MAGA DOGEbags (with or without their chainsaws), crypto-related policy is not a partisan issue. The policy discussion has moved beyond the question of whether bitcoin and crypto should be part of the broader financial market to the question of how the legal and regulatory infrastructure should adapt. The fact that Democrats and Republicans can find agreement to the point of advancing legislation together tells me that bitcoin and crypto are more resilient than any party or person in power.

So that’s the U.S.

Across the Atlantic, Europe’s MiCA grace period expired on July 1 and about 80% of the incumbent, pre-MiCA operators failed to get licensed. As a result, users of many smaller platforms in the EU are facing significant disruption — accounts frozen or wound down, assets that must migrate to a licensed provider or into self-custody, and a market that consolidates hard toward large, licensed players.

Across the Channel, the UK’s FCA published its final custody rulebook. Soon, holding crypto through a UK platform will bring defined legal protections, including a definition of what counts as custody. This will include “shadow custody,” in which a platform holds the keys and technically could control a user’s coins even if it promises to never do so, and guidance on what happens to a user’s coins if the platform fails.

As customers of FTX and other failed platforms have experienced, loss in fiat-denominated price is painful but survivable. But when the platform holds the keys and the platform fails — if the assets aren’t title-held by a “qualified custodian” — you stop being an owner and become an unsecured creditor. You might be lucky enough to recover a fraction years later, but very often you end up with nothing. (And in the case of public bankruptcies like Celsius, BlockFi, and FTX, loss of privacy by being doxxed in the public record as an unsecured creditor.)

I think that what’s more interesting than any particular policy is the trend of increasing legislative and regulatory guidance coming from three major jurisdictions, each of which is also navigating significant political fissures. Even as bitcoin flirts with the bottom of its 200WMA, the US, UK, and EU are building permanent legal infrastructure. On the surface these this might seem boring, but it’s a signal that the establishment believes the asset is here to stay.

Erosion of the Y-axis

I want to close this post with a mental exercise that I plan to return to in a future post.

The market is defined in fiat terms. We are accustomed to watching the value of assets rise and fall in the context of USD, GBP, EUR, and other fiat currencies. Of course, this makes sense because our financial commitments and the stuff we might want to buy are priced in those currencies. When candles are green and bitcoin is ripping, we feel great. We’re the smartest people in the world! When they’re red and we’re pounding out a market bottom, we feel sick, and we start to question our conviction.

There’s a kind of irony at play here. As all readers surely know, the Bitcoin network launched amid the Great Financial Crisis. Embedded in the Genesis block was Satoshi’s vote of no confidence in the Chancellor of the Exchequer and a repudiation of the politics behind bailing out banks that are “too big to fail”. Bitcoin offers a peer-to-peer electronic cash system and a form of finite money that gets harder over time.

The point of bitcoin was to create a form of money that doesn’t depend on government’s fiscal restraint. As long as rulers have issued currency, they have debased the money their subjects are required to transact in. Most bitcoiners recognize this fact; this is one of the driving factors of “number go up”. Much of the reason to want bitcoin is that the Y-axis it’s measured by is designed to lose value over time and in only seventeen years, that’s precisely what has happened.

If the Y-axis is steady and one dollar = “one dollar”, then bitcoin’s move from $60,000 to $125,000 is success and a move in the opposite direction is failure. But if the Y-axis takes into consideration the erosion of the value of each dollar, the analysis gets more nuanced.

“The value of the dollar” isn’t a simple calculation. There are at least two different lenses through which we can look at the issue. The first lens is the Consumer Price Index, or CPI. This is how you measure what a dollar buys at the grocery store or the gas station. Since January 2009 (the month of bitcoin’s genesis block) the CPI has climbed 59%. A 2009 dollar now buys about 63 cents of the same basket of goods. That’s significant value erosion, but perhaps it isn’t too dramatic.

The second lens is very different: how many dollars exist in the first place. That’s M2 — the broad measure of the money supply, everything from cash in your wallet to savings accounts to money market funds. M2 has grown 178% over the same period of time. Those two yardsticks — the 59% increase in CPI and the 178% increase in M2 — should make us scratch our heads for a minute. It’s the same seventeen years, same dollar, same economy. If the money supply grew three times faster than the cost of milk and gas, where did the difference go? (Clearly into things that don’t drive CPI, like investment assets, durable goods, etc.)

Whether we adjust the Y-axis using CPI or M2, bitcoin’s “value” has clearly outrun both. Since the start of 2020 — the era that printed nearly a third of every dollar now in existence — bitcoin has gone from about $7,000 to roughly $59,000 even after this drawdown. That’s about 8x, against a money supply that grew by almost half over the same period. Measured honestly against the M2 yardstick, the current “crash” is a rounding error on a chart doing exactly what Satoshi’s thesis predicted: bitcoin held its value while the dollar lost its own.

To be fair, my measuring-stick argument cuts both ways. Those who bought the top of the cycle in late 2021 are still underwater four years later, and no amount of M2 reframing changes this. Buying the froth of euphoria can punish you regardless of the denominator. But if we zoom out past any single cycle, the lesson is clear: it’s the dollar that has been reliably, consistently, and deliberately losing ground.

The broader point is that bitcoin’s original thesis remains very much intact. Its fixed, finite supply and its decaying token issuance rate is the expression of fiscal restraint manifest in code. This has not changed. It cannot be changed. Regardless of what bitcoin does against fiat or what fiat does against bitcoin, the essential value proposition of bitcoin as a monetary good becomes only more durable over time.

Although the Overton window has shifted toward bitcoin, the market is still quite immature. The market still generally treats bitcoin as a speculative “risk on” asset. Capital flows out to chase the latest meme (today it’s AI) and bitcoin goes red when global conflict and uncertainty rise. These aren’t bitcoin’s flaws; they’re just evidence that Mr. Market doesn’t yet really understand what bitcoin is and does.

Bitcoin has only been a mainstream investable asset since January 2024 when the ETPs went live in the U.S. Before then, people had to work hard to understand private keys, coordinate their banking, and navigate a much more complicated buying, holding, and selling infrastructure. In 2024 the U.S. markets had an exciting, shiny new toy to play with. In a heavily-contested election year, the crypto industry dumped hundreds of millions of dollars into the election market to promote its interests, surely influencing the narrative. With undeniable mastery of driving media narratives, the new administration patronized (leveraged, exploited) the nascent and enthusiastic (naive) bitcoin and crypto crowds (ultimately for the administration’s own pecuniary gain). This undoubtedly accounted for much of bitcoin’s market rally through 2024 and 2025. These are behaviors of an immature, speculative market, not of a resilient and enduring store of value. When most people still don’t know the difference between bitcoin and “crypto”, it’s understandable that they’ll trend the same way when risk sentiment shifts.

The fundamentals of bitcoin are unchanged regardless of how we measure the Y-axis. The value of the dollar will continue to erode against literally anything that’s scarce. This is an inevitability; the only question is how rapidly the value erodes.

Spot oscillation is an immediate-term distraction from a more important story. Bitcoin is testing its 200WMA again and every time, flirting with this line marked the turning of the cycle. But perhaps instead of focusing on short-term fiat price we should be looking at the Y-axis: the fiat measuring stick. We get distracted by measuring a finite asset with a fickle unit (the dollar) the government keeps devaluing and we blanch when we don’t like how bitcoin measures up. Whether it’s at $60,000 or $125,000, the core thesis behind bitcoin is unchanged. Fiat money is broken. It’s broken BY DESIGN. Perhaps our focus shouldn’t be bitcoin’s value against the dollar. Perhaps we should consider whether the dollar is a useful measuring stick at all.